Anchor points

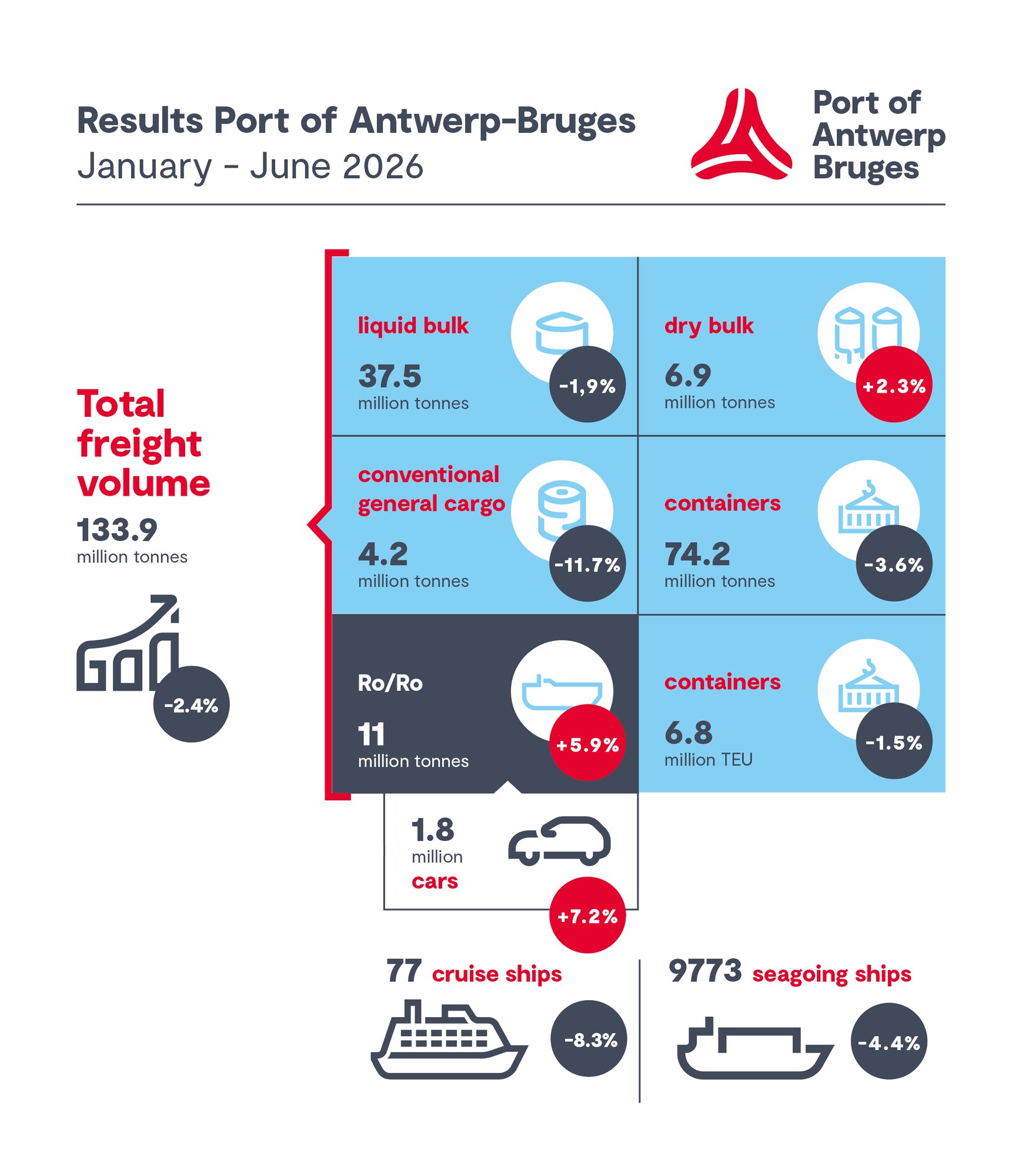

- Total cargo handling fell by 2.4% in the first half of 2026

- Geopolitical forces are reshaping trade flows

- Operational disruptions are impacting container throughput

- The market share of containers remains stable, and investments are bolstering the future

Container flows under pressure due to exceptional disruptions

Container throughput came under pressure in the first half of 2026 and was the main cause of the decline in total cargo handling. Expressed in TEU, throughput fell by 1.5% compared to an exceptionally strong first half of 2025; in tons, the decline was 3.6%. Exports of full containers in particular fell behind (-5.7%), reflecting the weak export position of the Western European economy. At the same time, throughput of empty containers rose (+13.7%), indicating a growing imbalance between imports and available export cargo.

The decline was exacerbated by exceptional operational disruptions. A four-day strike in the nautical chain in March resulted in an estimated loss of 100,000 TEU, followed by the oil spill in the Deurganck dock in April, which caused an additional loss of approximately 85,000 TEU. In June, industrial action by pilots once again caused disruptions and resulted in an estimated loss of 75,000 TEU. Despite diversions and adjusted sailing schedules, the port remained operational, and backlogs were gradually cleared.

Geopolitical forces are reshaping trade flows

The geopolitical developments in the Middle East had a clear impact on trade flows. Imports from the countries around the Persian Gulf were 57% lower in the first half of 2026 compared to the previous year. Energy flows above all were impacted: following the final LNG shipment from Qatar on 23 March, shipments from the region came to a virtual standstill in April, and LNG shipments from Qatar fell by 66%. Container shipping lines adjusted their schedules and plotted alternative routes through the Red Sea and the Eastern Mediterranean region. As a result, cargo flows through the Persian Gulf declined sharply, while other ports in the Middle East picked up the slack. Net cargo losses related to the Persian Gulf rose to approximately 2.2 million tons in the first half of the year. The biggest impact is indirect: higher energy, bunker, and transport costs, as well as disruptions to supply chains, are putting additional pressure on European industry.

U.S. trade policy also had an impact. The United States remained Port of Antwerp-Bruges’ most important trade partner, but imports of full containers from the U.S. fell by 10.4%, while exports to the U.S. fell by 16.5%. Exports of conventional general cargo to the U.S., primarily steel, fell by 32%. Conversely, liquid bulk increased thanks to higher volumes of LNG and chemicals. China is still a growth market, with higher container traffic, vehicle volumes, and steel shipments. LNG imports from Russia rose by 12.5% ahead of the European import ban which will come into force in 2027.

Other cargo segments showed resilience

Apart from container throughput, the other segments held up well. RoRo throughput grew by 5.9%, driven by higher volumes of new vehicles and unaccompanied cargo. The number of new vehicles handled rose by 7.7% to 1,695,000 units, mainly due to growth in China (+25.5%) and Japan (+5.5%). Bulk traffic also remained relatively stable. Dry bulk grew by 2.2%, while liquid bulk declined slightly (-1.9%) after a weak start to the year. There were significant shifts within this segment, including growth in LNG (+1.3%) and naphtha (+31.3%). Conventional general cargo remained under pressure (-11.7%) due to weak European industrial demand, U.S. import tariffs on steel, high energy and transport costs, and uncertainty surrounding the CBAM and European import quotas. The higher steel volumes from China (+44.8%) only partially offset the decline in other trade flows.

View the detailed annual figures

Market share of containers remains stable, investments are bolstering the future.

Despite the challenging market conditions, Port of Antwerp-Bruges was able to stabilise its market share. Furthermore, new developments within the container alliances strengthened its position. For example, Gemini Cooperation took the decision to deploy deep-sea services to Antwerp on the Far East–Europe trade lane, while Premier Alliance deployed larger container vessels. Important steps were also taken toward developing the Extra Container Capacity Antwerp (ECA) project, with the market assessment for the allocation of additional container capacity and the Flemish government’s approval of the draft project decision for the Left Bank Container Cluster (CCL). By investing in capacity, efficient infrastructure, and sustainable logistics, Port of Antwerp-Bruges continues to strengthen its position as a dependable gateway to Europe.

Rob Smeets, CEO of Port of Antwerp-Bruges: “The first half of the year shows that Port of Antwerp-Bruges continues to play its role as a gateway to Europe, even in exceptional circumstances." Trade flows are continually adapting to the new geopolitical reality. This demands flexibility from our port community and underscores the importance of continued investment in capacity, efficient infrastructure, and sustainable logistics. At the same time, the international context remains extremely uncertain. That is why Europe must continue to focus on a strong industrial policy and a competitive investment climate.

”

Johan Klaps, Chairman of the Board of Directors of Port of Antwerp-Bruges and Port Alderman for Antwerp: “The first half of this year demonstrates not only how vulnerable international logistics chains are to disruptions, but also how resilient our port is. Despite successive operational challenges, Port of Antwerp-Bruges managed to maintain its market share in container traffic. This confirms just how crucial investments in accessibility and capacity, as well as a reliable port organisation, are to our port’s appeal to shipping lines, the industry and the wider logistics sector.

”

Dirk De Fauw, Vice-Chairman of the Board of Directors of Port of Antwerp-Bruges and Mayor of Bruges: “The rapid shift in energy flows demonstrates how essential the complementarity between Antwerp and Zeebrugge is.” Thanks to this complementarity, our port remains a crucial link in Europe’s energy and logistics supply chains. By continuing to invest in infrastructure and sustainable growth, we are not only strengthening the port, but also boosting economic vitality and employment in our region.

”